Strong investments and operational excellence: EOS Group concludes successful fiscal year

Hamburg, July 22, 2026

- EOS Consolidated increases earnings to EUR 464.0 million (EBITDA).

- Substantial investments of EUR 1 billion in receivables portfolios drive growth.

- Outstanding ESG rating with EcoVadis Gold Medal confirms successful sustainability strategy.

The EOS Group has confirmed its strong position in the European market and concluded fiscal year 2025/26 with renewed growth. Earnings before interest, taxes, and depreciation (EBITDA) of EOS Consolidated rose to EUR 464.0 million (prior year: EUR 460.8 million). Revenue increased by 1.4 percent to EUR 1.1 billion.

Substantial investments in receivables portfolios were the primary driver of the successful fiscal year. In total, EOS Consolidated invested EUR 1 billion in unsecured and secured receivables, as well as REO* portfolios (prior year: EUR 826.6 million). This represents an increase of more than 20 percent compared to 2024/25. Significant investments were made in France, Germany, Portugal, Poland, and Romania. EOS also acquired decisive portfolios in smaller markets such as North Macedonia, Slovakia, Bulgaria, and Belgium. "We have achieved the second-highest investment volume in EOS Group's history after the record year 2022/23. For European banks, EOS Group is a reliable partner for the sale of their non-performing loan (NPL) portfolios," says Marwin Ramcke, CEO of the EOS Group.

*REO stands for real-estate-owned

Growth in Western Europe

EOS Group further strengthened its market position in Western Europe in fiscal year 2025/26 and increased revenue to EUR 318.9 million (+6.6 percent). Particularly high investments in unsecured receivables portfolios in France and Portugal drove this growth. In total, EOS Consolidated invested EUR 382.8 million in receivables portfolios in Western Europe. "We achieved consistently strong results in both smaller and larger Western European markets. This success was also driven by our focused progress in receivables management software, digital service portals, and process optimizations through AI," says Sebastian Pollmer, member of the EOS Group's Board of Directors, responsible for the Western European region.

Strong position in Eastern Europe confirmed

In Eastern Europe, EOS Group generated revenue of EUR 372.8 million and invested EUR 361.6 million in receivables portfolios – a 16 percent increase in investments compared to the prior year. Significant NPL portfolio acquisitions in Poland, Romania, Bulgaria, and Greece characterized the fiscal year. "Our success in Eastern Europe is driven by strong operational performance and intensive cross-border collaboration among our employees," emphasizes Carsten Tidow, member of the EOS Group's Board of Directors and responsible for Eastern Europe. The region also benefited from the strategic use of technology, such as pilot projects with Agentic AI.

Investments increased in Central Europe

Central Europe is EOS Group's highest-revenue region with EUR 376.2 million in revenue. Investments in NPLs and real estate increased to EUR 256.3 million. Particularly noteworthy are large portfolio acquisitions in Germany. EOS also strengthened its competitive position in Slovakia and Slovenia through the acquisition of unsecured receivables portfolios and investments in bridge loans. "Given the mature and highly competitive markets in Central Europe, we are particularly pleased with the substantial investments in Germany, one of EOS Group's most important markets," explains Dr. Stephan Ohlmeyer, member of the EOS Group's Board of Directors, responsible for the Central European region.

High resilience through diversification

The EOS Group is active in over 20 European markets and benefits from broad diversification. "Our focus on diverse markets makes our company more resilient and, in light of current geopolitical challenges, ensures broader risk distribution," says Dr. Eva Griewel, CFO of the EOS Group. "The exchange among our local experts enables us to develop innovative solutions across the Group."

This includes the strategic use of artificial intelligence and the automation of repetitive tasks. Also, the continuous advancement of the proprietary receivables management software Kollecto+ in now 13 countries delivers measurable results.

Recognition for sustainability performance

For EOS, the entire value chain – from the acquisition of non-performing receivables to debt relief of defaulting payers – is inseparably linked with responsible business practices. Following the Bronze Medal in the prior year, EOS Holding received the Gold Medal from EcoVadis in fiscal year 2025/26. EOS now ranks among the top five percent of the world’s most sustainable companies and the top three percent in its industry. "Sustainability is an integral part of our business model and a clear signal to our partners," emphasizes CEO Marwin Ramcke.

The EOS Group's Annual and Sustainability Report provides comprehensive insights into the company’s achievements in this area.

About the EOS Group

The EOS Group is a leading technology-driven investor in receivables portfolios and an expert in the processing of outstanding receivables. With over 50 years of experience and offices in more than 20 countries, EOS offers smart services for receivables management worldwide. Its key target sectors are banking, real estate, telecommunications, utilities, and e-commerce. EOS employs more than 6,000 people and is part of Otto Group.

For more information on EOS Group: eos-solutions.com

One in nine Slovaks with overdue payments borrows for holidays

The representative survey, conducted by the AKO agency, found that 11.3% of respondents with overdue payments admitted to borrowing money to finance a holiday.

This figure is higher than borrowing for purchases often considered essential, such as electronics, healthcare, or even groceries. The findings highlight a growing pressure to maintain a certain lifestyle, even at the expense of financial stability.

"In many cases, holiday loans are not driven by necessity but by a desire for a lifestyle that is currently out of reach," notes Peter Čanda, a manager at EOS KSI Slovakia. "This is a notable trend of our time, fueled by advertising and social media, where a short-term experience is financed at the expense of future financial security."

Holiday borrowing varies by age, gender, and region

The EOS KSI Slovakia survey results show which groups are more likely to take on debt for a holiday:

- Gender: Men are twice as likely as women to borrow for this reason.

- Age: Young people aged 18 to 33 are a key group, with approximately one-fifth borrowing for a holiday. The second highest-risk group are those aged 50 to 65, even though their primary debts are often related to housing.

- Region: There are significant regional differences, with the Žilina region showing the highest rates of holiday-related borrowing.

Middle-income households and single parents feel the most pressure

The pressure to fund a holiday is most acute among middle-income households. Approximately three out of ten defaulting payers with a net monthly household income between €1,401 and €1,800 borrowed for a holiday. For those earning between €1,801 and €2,500, this figure rises to four out of ten.

In contrast, households with a monthly income below €1,000 or above €2,501 reported no borrowing for holidays. This suggests that economically sensitive middle-income households feel the greatest pressure to take a holiday, even if it leads to financial strain.

For single parents with one child, a holiday loan is the most frequent cause of overdue payments. This group is not only the most likely to struggle with overdue payments, but 64% also report feeling stress or anxiety about their financial situation.

Why a holiday loan can be a financial risk

Interestingly, the rate of borrowing for holidays is similar across people with basic and university-level education. This suggests that financial decisions are often influenced more by a lack of financial awareness than by the level of education.

"We see that borrowing is often driven by a desire to keep pace with one's social circle. In these cases, a holiday becomes a matter of status," explains Peter Dvornák, CEO of EOS KSI Slovakia.

A short-term break can have long-term financial consequences. While the holiday itself lasts only a few days, loan repayments can stretch over months or even years, often with high interest rates.

"Taking a break is important for well-being, but it should never threaten the financial stability of an individual or a household," advises Peter Dvornák. "It is far more sustainable to choose a more affordable option, plan, and build a savings fund rather than borrowing and risking unmanageable debt."

Overdue debts negatively affect relationships and family

More than a quarter of indebted Slovaks, as many as 27.9 percent, admit that overdue debts negatively affect their relationships with family and friends. This is according to a survey by the collection company EOS KSI Slovensko, conducted by the AKO agency.

Every tenth debtor struggles with feelings of depression, and 8 percent experience stress, nervousness, or fear. More than 12 percent of respondents directly confirmed that their overdue debt has damaged their interpersonal relationships, with almost 8 percent experiencing constant arguments and 4.2 percent losing the trust of their loved ones.

Authentic statements from respondents who decided to speak openly about their feelings and family relationships affected by overdue debts:

"I'm hiding it so they don't know, and it's weird. The family is pressuring for payment and makes it quite clear that one is irresponsible in this matter. It was a tense situation; I had nothing to pay with and had to borrow for the installments. In everyone's eyes, I was insolvent, irresponsible. My family blames me for my mistake and wants to disinherit me. Since I'm nervous, I tend to be unpleasant to them. I have depression, I sleep poorly, I can't handle it. If I died, they would have to pay it off for me. I can't even go on a small one-day trip with my son. I'm afraid to spend even one cent on myself when everything is expensive. I refuse all invitations to family celebrations so I don't have to buy gifts because I have to pay off debts, I don't celebrate any of my own holidays, and I don't invite any family over because I can't afford to host even the closest family."

Overdue debts are therefore not just a financial problem. "It is important to pay attention to financial literacy and preventing the creation of bad debts," states Peter Dvornák, director of EOS KSI Slovensko. A bad debt could be, for example, paying for a holiday that exceeds an individual's financial means.

Debts weigh most heavily on those who live with family

The survey results also showed that the relationship impacts of debt vary significantly by household type. The most vulnerable groups are single parents with one child – up to half of them confirmed that debt negatively affects their family life. An even higher proportion, 52 percent, was reported by adults living with their parents without financially contributing to the household.

"For adults living with their parents, a feeling of dependency and reproach often accumulates, which can deepen tension and disrupt relationships. Single parents, on the other hand, bear the entire financial burden alone and live in a sensitive situation where every expense puts pressure on the budget," states Executive Manager Peter Čanda.

People with basic education from the Prešov and Trenčín regions are most affected by the disruption of relationships caused by overdue debts. Surprisingly, it is not always just people with the lowest income. Negative impacts are also reported by households with an income of up to 1800 euros.

Why a holiday is a bad debt and what to do about it

As many as 11.3 percent of respondents with debts admitted to borrowing specifically for a holiday. However, a short-term break can have long-term financial consequences. While the holiday experience itself lasts only a few days, repaying the loan can stretch over months, sometimes even years – often with high interest rates.

"Resting on holiday is important for mental health, but financing it should not jeopardize the financial stability of the individual or the entire household. It is much more sensible to choose a cheaper alternative, plan ahead, and build up a financial reserve than to borrow and later face the risk of indebtedness or debt traps, and the associated pressure on relationships and mental health," advises Peter Dvornák, director of EOS KSI Slovensko, in conclusion.

SUMMARY

Respondents who acknowledged the impact of debt reported several negative effects:

- Internal feelings: 10% feel depression, 8% stress, nervousness or fear, 4.2% a sense of exclusion, 1.9% shame, and 0.4% dependency.

- Disruption of relationships: 12.6% of respondents confirmed a general disruption of relationships, 5.4% worsened relationships, and 4.6% a significant impact on interpersonal relationships.

- Communication problems: 7.7% experience constant arguments, 3.1% feel that their loved ones do not talk to them, and 1.1% reported worsened communication.

- Loss of trust: 4.2% of respondents admitted to a loss of trust from their loved ones due to debt.

Respondents' reactions:

- Agreement with the statement "My overdue debt affects my relationships with family and friends": 27.9%. Above-average agreement was expressed mainly by younger people aged 18–49, men, people with basic or secondary education without a high school diploma, and respondents from the Prešov and Trenčín regions. A stronger representation of affirmative answers was recorded in households with lower income (up to €1800), single parents, and adults living with their parents. Two-thirds of people with overdue debts agree with this statement.

- Disagreement: 34.7% disagree completely.

- Uncertainty: 17.8% of respondents could not say.

Every tenth Slovak in debt enforcement wants to transfer their property to a relative

Increasing income by finding a second or third job, personal bankruptcy, but also transferring property to family or moving abroad to escape debt enforcement. A survey by the collection company EOS KSI Slovensko shows that the approaches of people affected by debt enforcement are diametrically different, including between men and women.

More than half of the respondents, 56.2 percent, when asked 'How should people affected by debt enforcement behave,' chose increasing their income by finding another job and paying off the debt as their first choice. This applies to 58% of the women and 54% of the men surveyed, young people up to 33 years old, more educated population groups, rather higher-income categories, and those with savings.

Women behave more responsibly and actively solve problems

In second place for solving debt enforcement, the survey revealed an attempt to get out of debt through personal bankruptcy. This solution is preferred by 43 percent of respondents, more often men, middle-aged categories from 34 to 65 years, residents of the Banská Bystrica region, people from multi-generational households, and adults living with relatives who share costs. Here too, women showed themselves to be greater fighters: 37% of female respondents would choose personal bankruptcy, compared to almost half, 49%, of male respondents.

"Men look for simpler solutions such as personal bankruptcy or fleeing abroad from debt enforcement, while women behave more responsibly and actively solve the problem," interprets Václav Hřích, director of the research agency AKO.

Every tenth respondent, i.e., 10.5 percent, would solve a debt enforcement situation with a loan from family, and approximately every tenth respondent, 10.2%, would not look for another job, would not choose personal bankruptcy, nor borrow from family, but would try to transfer their property to a close relative or friend.

Moving abroad or 'invisibility' are not good solutions

Among other solutions that people in debt enforcement would use is moving abroad. Some respondents even openly stated that they would try to act 'invisibly' and not respond. The tendency to flee from debts was declared in the survey more by younger age groups from 18 to 33 years.

"Not responding, not communicating, or moving abroad to live is definitely not the right way to resolve your obligations. In today's world of interconnected information systems, it is no longer possible to exist unidentified even abroad; the debt will catch up with you sooner or later. It is better to approach debts actively, communicate, and agree on a payment plan," concludes Peter Dvornák, CEO and Executive Director of EOS KSI Slovensko, summarizing the survey results.

Up to 75 percent of single parents with two or more children have no savings. This is according to a representative survey by EOS KSI Slovensko, conducted by the AKO agency. They have no savings and feel they are worse off than a year ago. This population group also confirms problems with repaying their obligations and debts.

Single parents with one or more children are unable to build a financial reserve. Two-thirds of single parents (mothers or fathers), according to the survey results, have no savings. In the category of single parents with two or more children, this figure is as high as 75 percent. In contrast, up to 67 percent of seniors aged 66 and over declare that they have savings.

"This doesn't mean that seniors in our country are well off. However, it is clear that mothers or fathers who are raising children on their own are the most vulnerable social group," analyzes Peter Dvornák, CEO of the collection company EOS KSI Slovensko.

Even single parents who do have some savings admit they are minimal. The majority (38 percent with one child, 67 percent with two or more children) have an amount up to 1000 EUR, and only in a smaller number of cases (26% with one child, 33% with two or more children) does it exceed 5,000 EUR.

"If this group's situation unexpectedly worsens or they lose their job, for example, they almost immediately fall into the state's social safety net. In many cases, however, even that cannot help them live a dignified life," explains Peter Čanda, Executive Manager of EOS KSI Slovensko.

Their situation is getting worse year by year

According to the EOS KSI Slovensko survey, two-thirds of single parents with one child and 42 percent with two or more children feel that their financial situation has worsened year-on-year. In comparison, 36 percent of people aged 66 and over rate their financial situation as worse. More than half of them consider it unchanged. "This indicator shows that the recent indexation of pensions has outpaced inflation, and seniors also feel the thirteenth pension. However, state aid for single parents has not grown at a similar rate," clarifies Václav Hřích from the AKO agency about the possible causes.

According to the latest census, there are approximately 200,000 single-parent households in Slovakia on the poverty line. The non-profit organization Jeden rodič (One Parent) explains that it is a trap the system has put them in, and from which they have no chance of getting out on their own.

Debts and repayment problems

Only 11 percent of seniors aged 66 and over currently have a loan or overdue receivables, but up to 60 percent of single parents with one child do. Compared to the general population, a high percentage of single parents (10 percent with one child, 25 percent with two or more children) are unable to pay their obligations on time. In the total population, only 4.4 percent of survey respondents have overdue debts, and among seniors over 66, only one percent of people have unpaid debts.

"If a single parent has an obligation with us that they cannot manage to repay, they just need to contact us. We have already helped thousands of debtors," says Peter Dvornák, Director of EOS KSI Slovensko, suggesting a way to solve the problems, and adds: "There is no one-size-fits-all solution for everyone, but we will certainly find a suitable procedure for a specific debtor, taking into account their difficult life situation."

Up to 54.6 per cent of the Slovak population has a poor estimate of their ability to pay at the onset unmanaged debts. This is according to a survey conducted by AKO for EOS KSI Slovakia. What to do so that the bailiff does not come after Baby Jesus?

Poor estimation of solvency when incurring unmanageable debts is more often reported by men; university graduates educated; with an income above EUR 1,001; in the municipal regions of Bratislava, Trnava and Žilina; independently living in the region; those who currently have loans; those who have had no problem paying their debts on time.

"The generous gifts that are bought during the Christmas holidays for loved ones bring joy, but they are also a source of financial stress. It is not difficult to prepare a lavish gift under the tree in an effort to succumb to the temptation to buy gifts on credit. And so it is not difficult nowadays to make problematic debt by recklessly borrowing for things we can do without in life." points out Andrea Slezáková, dedicated to financial literacy at EOS KSI Slovensko.

This is confirmed by the AKO survey for EOS KSI Slovensko, where, when asked what the main reason of debt repayment problems is, answered by a representative sample of 1,000 adults’ respondents as follows:

- 45.4% Irresponsible financial behaviour

- 44.2% Incorrect prioritisation

- 43% Low financial literacy

Good and bad debt

Borrowing to buy unnecessary Christmas presents may therefore not always be a good idea.

"If it's a long-term investment in housing, for example to buy kitchen units or photovoltaic panels or to buy an appliance that you really need in the home, if it's an investment in health or education, such as buying a laptop, or buying a useful item with a long durability, in such cases it makes sense to borrow," says Andrea Slezáková, adding that in this case, it is the so-called good debt.

Paying for a luxury holiday on debt or the latest type of mobile phone are bad debts and do not make sense - points out Peter Dvornák, Executive Director of EOS KSI Slovensko. "The pressure on the general pre-Christmas spending is more a result of social expectation, not the need for festive survival. The golden rule of financial literacy says that the repayment period should not exceed the lifetime of the item you are buying," he concludes.

Advice in conclusion

When buying (not just a Christmas present) on debt, it's important to be good at calculating whether the family budget will be sufficient to meet the repayments over the life of the loan, and what the total cost of the loan will be. However, if by changing life situation causes problems in meeting the repayment terms, it is important to discuss the debt communicate with the competent authority, institution, individual and make arrangements for both parties an acceptable to comfortable change of the repayment schedule or rules.

The AKO survey for EOS KSI Slovakia was carried out on a representative sample of 1,000 adult respondents using the method CAWI (online panel) data collection, 2023.

Media contact:

Mobile: +421 907 8210

Mail: [email protected]

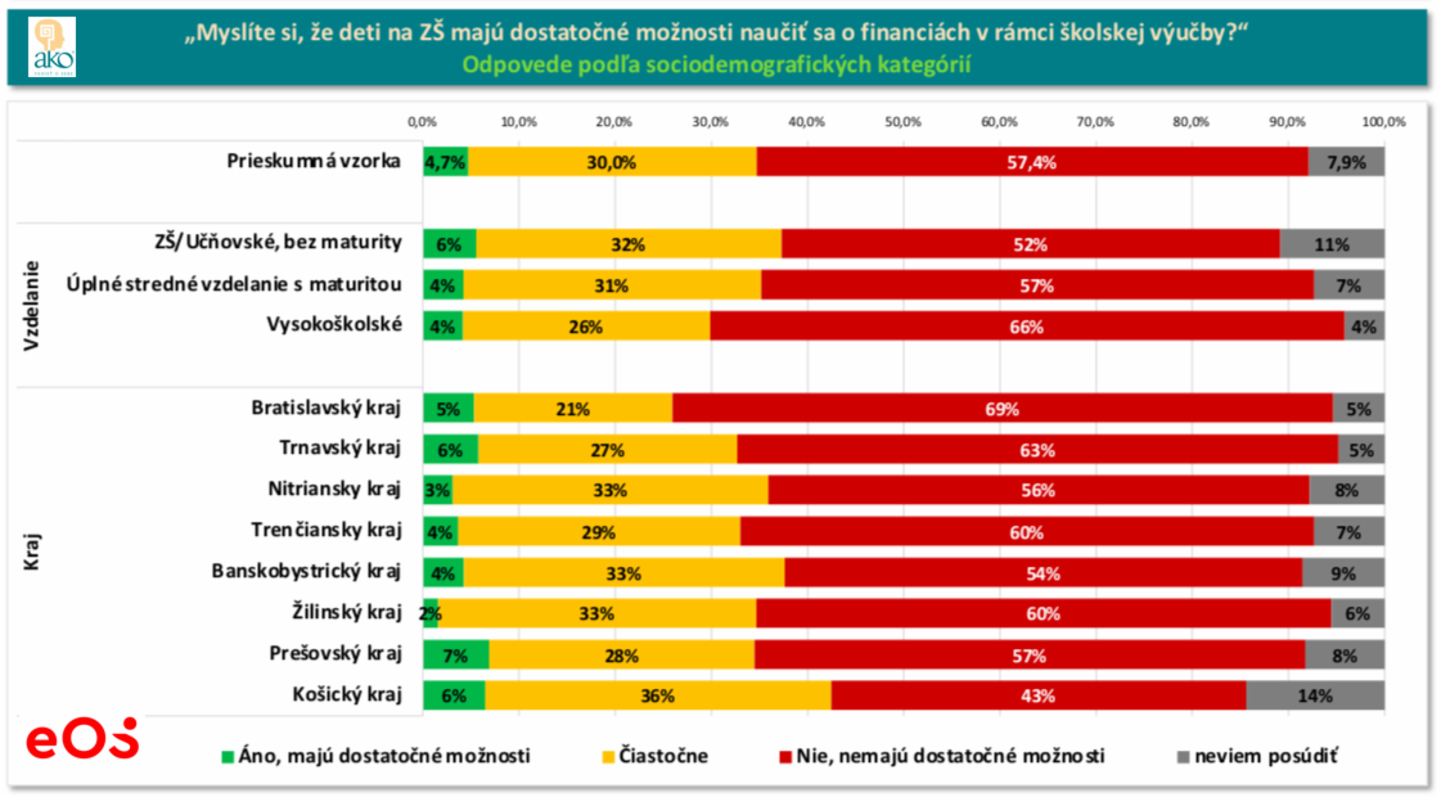

57 per cent of Slovaks think that financial education at primary school is insufficient.

Bratislava, 20.9.2023

57.4 per cent of the adult population describe the opportunities to learn about finance in primary school as insufficient. Three out of ten Slovaks surveyed consider these opportunities to be partially sufficient and only one in twenty respondents, or 4.7 per cent, consider them sufficient.

The data are the result of a recent survey conducted by EOS KSI Slovensko in cooperation with AKO.

"This is an alarming state of affairs," says EOS KSI Slovensko Managing Director Peter Dvornák."Financial literacy from school age promotes the ability to manage responsibly and optimally handle finances in everyday life in adulthood," he points out.

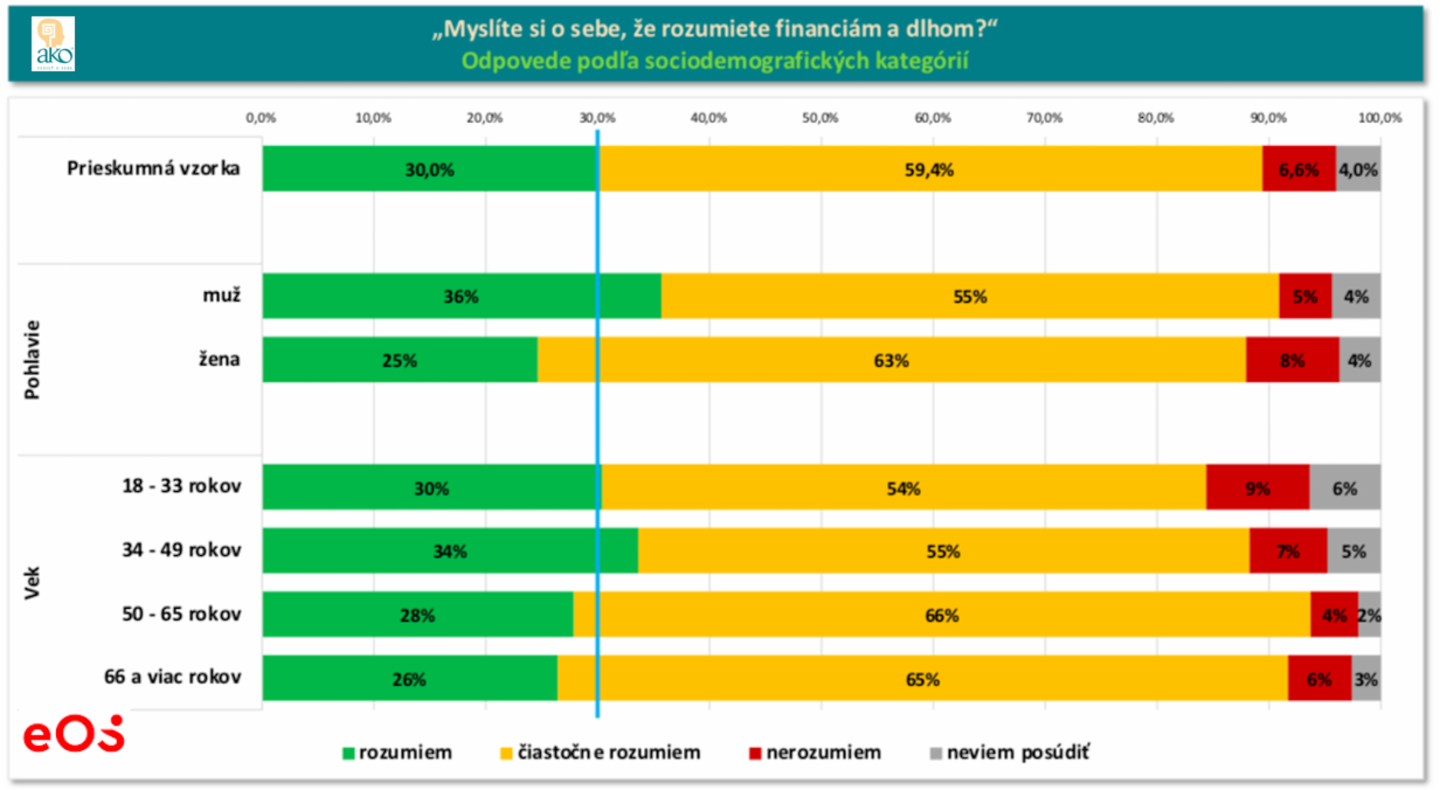

The survey also shows that even 6 out of 10 Slovak adults are not confident about their knowledge of finances and debt. Almost 60 per cent (59.4) of Slovak adults gave a verbal answer to the question "Do you think you understand finance and debt": "Partially." 6.6 percent of respondents admitted that they did not understand the issue at all, and 4 percent could not judge.

"We should always keep in mind that we need to educate ourselves, because no one will take care of our money better than ourselves," says Andrea Slezáková, expert guarantor of the volunteer financial education project under the auspices of EOS KSI Slovensko, adding that: "Those who understand money are ultimately able to keep it."

The level of teaching children in primary school about finance is perceived as insufficient above average by: young people aged 18-33 (68%); seniors 66 plus (60%); people with an income of over €1,200; people residing in the Bratislava and Trnava regions; Slovaks who have never had debts to companies or institutions (not family and friends) (63%), as well as those who currently have loans (61%).

Experts in the field of financial education have experience that children as early as 4th grade of primary school are able to understand and work with the issue if it is presented appropriately. "It is therefore advisable to discuss finance with children actively at classroom (teacher-student) level and in the home. This paves the way for a better perception of the value of money and more effective financial decisions in the future," concludes EOS KSI Slovakia Managing Director Peter Dvornák.

More about the basic principles of financial literacy in the podcast at: bit.ly/3r9YeTw

The survey was conducted on a representative sample of 1,000 adult respondents using the CAWI (online panel) data collection method in the second quarter of 2023.

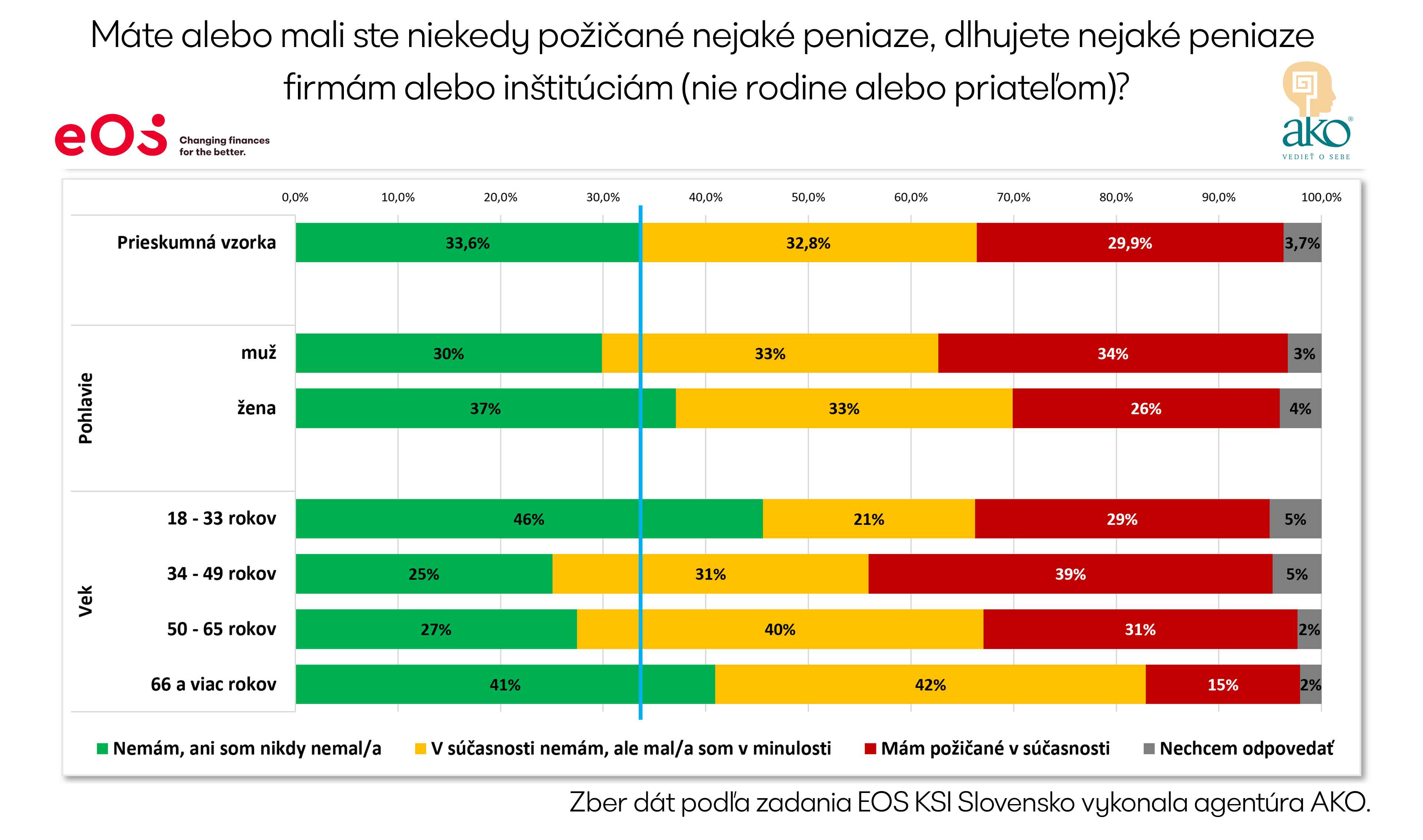

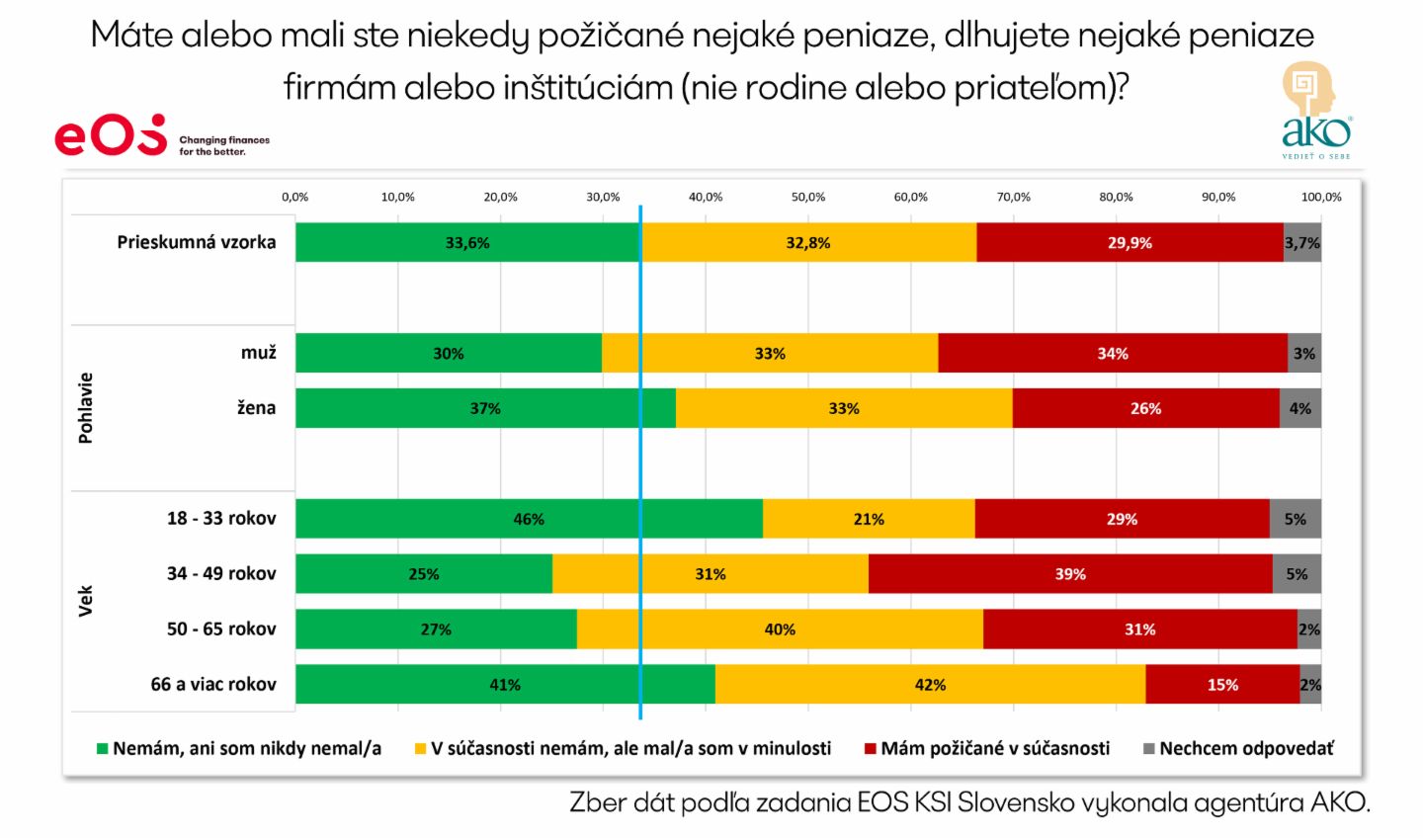

AKO survey on Slovaks and their debt: 6.6% of Slovaks have debts that they cannot repay, young families are the most indebted, older people repay better.

Bratislava, 17.3.2023

Up to 6.6 per cent of the adult population in the Slovak Republic is unable to repay its debts. This is according to a recent survey conducted by EOS KSI Slovensko in cooperation with AKO.

"This is an alarming figure," warns Václav Hřích, director of AKO, because in these cases it is not only people who fail to pay their loans, but also, for example, their housing, energy, water and telecommunication bills, and they are borrowing even to buy basic necessities for their families. EOS KSI Slovakia Director Peter Dvornák confirms the overlap between the survey figures and reality: "The group aged 34 to 49 with young children is above average in failing to pay their debts. This is logically related to the effects of inflation and the fact that this is the most heavily indebted age group."

Roughly 7% (approx. 289 thousand) of the population over 18 years of age admitted that they do not understand the area of finance and debt at all. Only three out of 10 understand the issue and two thirds of those surveyed understand it partially. Debt was defined in the survey as any overdue obligation to a bank, leasing company, instalment sale or supplier of services such as electricity, gas, water, telecommunications or insurance.

Residents of the Bratislava region, which is also the richest, are more likely to pay their debts on time. The largest number of indebted people live in the Trnava and Trenčín regions.

Higher levels of debt understanding were declared by university educated people, men, the age group from 34 to 49 years, residents of the Bratislava and Prešov regions, people with higher incomes, couples with children, as well as single people. Low understanding of finances and debts was declared by women, people in the age group of 18 to 33 years, respondents with primary or apprenticeship education, people with income up to EUR 300, people living with relatives without a share of household costs.

Families with children and people with the lowest incomes are more likely to have repayment problems. Depending on the type of household, the most likely to repay are couples without children who have no family expenses. Similarly, single people have a stronger payment discipline.

"Many younger people with decent incomes and higher education have racked up higher loans. The standard of living for this group included having two cars in the family on lease, a high mortgage, or an investment loan in an investment property," offers EOS KSI Slovensko Director Peter Dvornák in explanation of the data. Corresponding to this assumption is the finding that young people approach the need for credit as a wise decision that will help them acquire assets and invest well.

In contrast to the young in their attitudes to debt is the group of seniors over 66, for whom the fact that they have debt would probably be a feeling of shame.

The survey was conducted on a representative sample of 1,000 adult respondents using the CAWI (online panel) data collection method between May 18 and June 2, 2023.

Bratislava, 17.3.2023

Vyplýva to zo záverov spotrebiteľskej štúdie EOS, do ktorej sa zapojilo 7 700 Európanov vrátane SR

- Inflácia a náklady na energie sú hlavnými dôvodmi vzniku nových dlhov

- Slováci výraznejšie využívajú kreditné karty a sú zvyčajne zadĺžení nad 10-tisíc Eur

- Väčšina Európanov má starosti o svoju finančnú budúcnosť

- Spotrebitelia šetria najmä na cestovaní, návštevách reštaurácií a novom oblečení

Prudko stúpajúca miera inflácie a energetická kríza viedli k zvýšeniu vnímania cien u väčšiny Európanov (53 percent). Približne pätina z nich si za posledných šesť mesiacov zobrala nové úvery. Toto je výsledok aktuálnej reprezentatívnej štúdie „Európania vo finančných problémoch?“ EOS Consumer Study 2023, do ktorej sa zapojilo 7 700 spotrebiteľov z 13 európskych krajín vrátane Slovenska.

Spotrebitelia vo východnej Európe sú v priemere zasiahnutí novými dlhmi viac

Najmä v krajinách východnej Európy spotrebitelia venovali v posledných šiestich mesiacoch zvýšenú pozornosť svojim výdavkom. Respondenti prieskumu uvádzali, že šetria najmä na cestovaní, na kultúrnych a voľnočasových aktivitách (po 33 percent), ale aj na novom oblečení (28 percent). Približne každý piaty z nich si však za posledných šesť mesiacov zobral nové úvery. Hlavnými dôvodmi tohto rozhodnutia boli inflácia (49 percent) a zvýšené náklady na energie (27 percent).

Vo východoeurópskych krajinách ako Rumunsko a Maďarsko (po 30 percent), ako aj v Severnom Macedónsku (29 percent) a v Srbsku (28 percent), sa nové úvery čerpali častejšie ako je európsky priemer. Slováci preferovali úverovanie aj kvôli bývaniu. Obyvatelia západnej Európy sa častejšie zadlžovali kvôli dovolenkám (18 percent), najčastejšie si však brali úvery na kúrenie a elektrinu (28 percent).

“Zadlžujeme sa, aby sme dokázali zaplatiť základné životné náklady. V krajinách východnej Európy vzniká až 28 percent dlhov preto, že ľudia nemajú prostriedky na uhradenie účtov za elektrinu a kúrenie. Špeciálne na Slovensku narástol počet používateľov kreditných kariet. Obzvlášť v tejto neľahkej dobe je treba mať na pamäti, že najzraniteľnejší spotrebitelia sú tí, ktorí precenia svoje finančné možnosti a kapacity. Platí však, že aj v najzložitejšej situácii je možné komunikovať o svojich dlhoch a hľadať účinné riešenia,” upozorňuje vzhľadom k číslam prieskumu konateľ EOS KSI Slovensko Peter Dvornák.

Ide o riešenia šité na mieru neplatiaceho spotrebiteľa, napríklad prostredníctvom spoločných dohôd o splátkach a výške jednorazových platieb.

Inflácia je najväčšou obavou do budúcnosti

Štúdia ukazuje aj zmenu vo využívaní platobných metód. Slováci začali masívnejšie využívať nielen kreditné karty, ale aj hotovosť. 42 percent respondentov z celej Európy uviedlo, že za posledných šesť mesiacov využívalo hotovosť častejšie ako predtým. Výsledok je prekvapujúci najmä vo vekovej kategórií 18 až 34-ročných, z ktorých takmer polovica používala hotovosť častejšie.

Vysoká inflácia a prudko rastúce náklady na energie vedú k finančným obavám takmer u troch štvrtín opýtaných spotrebiteľov (73 percent). Obavy z nezamestnanosti trápia najmä ľudí vo veku 18 až 34 rokov.

„Štúdia ukazuje, že inflácia nezostáva bez vplyvu na spotrebiteľov,“ hovorí Marwin Ramcke, generálny riaditeľ skupiny EOS. „Najmä v časoch krízy sa dlhom často nedá vyhnúť. Dokážu preklenúť krátkodobý nedostatok a dokonca zachrániť existenciu. Ako jednej z popredných spoločností na vymáhanie pohľadávok v Európe je pre nás dôležité poskytnúť spotrebiteľom férovú podporu pri splácaní ich dlhov, čo pomáha nielen im osobne, ale aj ekonomike, do ktorej sa peniaze vracajú,“ uzatvára.

O štúdii

Spotrebiteľská štúdia skupiny EOS „Európania vo finančných problémoch?” vznikla v spolupráci so spoločnosťou Dynata medzi 3. a 9. februárom 2023. Išlo o prieskum medzi 7 700 spotrebiteľmi v 13 európskych krajinách formou online dotazníka. Pozornosť sa sústredila na otázku, ako posledných 6 mesiacov ovplyvnilo vlastné správanie vlastnú finančnú situáciu.

O skupine EOS

Skupina EOS je popredným technologickým investorom do portfólií pohľadávok a expertom na spracovanie nesplatených pohľadávok. S viac ako 45-ročnými skúsenosťami a pobočkami v 25 krajinách ponúka EOS svojim približne 20 000 zákazníkom po celom svete služby inteligentnej správy pohľadávok. Zameriava sa na banky a spoločnosti z oblasti nehnuteľností, telekomunikácií, dodávok energií a elektronického obchodu. EOS zamestnáva viac ako 6000 ľudí a je súčasťou skupiny Otto Group.

Bratislava, 24. 7. 2019

Percento platieb načas je medzi európskymi firmami z roka na rok vyššie, no Slovensko v tomto ukazovateli výrazne zaostáva. Kým v roku 2014 firmy v Európe uhrádzali faktúry v stanovenom termíne v 75 percentách prípadov, vlani to už bolo 79 percent. Takéto závery priniesla reprezentatívna štúdia „European Payment Practices 2018“ skupiny EOS. Na Slovensku sa faktúry včas platia len v 73 percentách prípadov.

Žiadna iná krajina zo sledovaných krajín v rámci štúdie nezaznamenala nižšie percento platieb načas za rok 2018 než Slovensko. V Bulharsku to bolo 76 percent, vo Veľkej Británii 75 percent, zhodne po 74 percent úhrad načas mali krajiny ako Grécko a Rumunsko.

„Dopadnúť úplne najhoršie spomedzi sledovaných európskych krajín pri úhradách v stanovenom termíne je pre Slovensko zlou vizitkou. Najmä, ak si zoberieme, že trend v tomto ukazovateli sa v rámci celej Európy od roku 2014 až po súčasnosť vyvíja pozitívne,“ poznamenáva Michal Šoltes, konateľ spoločnosti EOS KSI Slovensko.

V prípade meškajúcich platieb odporúča zveriť sa do rúk profesionálov v oblasti správy a manažmentu inkasa pohľadávok.

O prieskume „European Payment Practices“:

Prieskum skupiny EOS s názvom „European Payment Practices“ (Európske platobné postupy) analyzuje vzťahy medzi platobnými zvyklosťami, podmienkami a vplyvom peňažných tokov na európsku ekonomiku a spoločnosť. Nezávislý inštitút pre prieskum trhu Kantar TNS na jar 2018 opäť v mene skupiny EOS oslovil odborníkov z európskych krajín v rámci prieskumu a opýtal sa ich na miestne platobné zvyklosti.

Tento prieskum je jedinečný, nielen čo sa týka množstva – 3 400 spoločností v 17 európskych štátoch, ale aj pokiaľ ide o zameranie na firemnú klientelu. Predmetom analýzy sa stali názory odborníkov na manažment pohľadávok zo spoločností, ktoré majú ročné príjmy v priemere 28 milión eur s počtom zamestnancov 180.

Na otázky o svojich skúsenostiach s platbami, hospodárskom vývoji krajiny a rizikách v manažmente pohľadávok odpovedalo po 200 firiem z Veľkej Británie, Španielska, Francúzska, Dánska, Grécka, Rumunska, Ruska, Slovenska, Bulharska, Poľska, Maďarska, Chorvátska, Slovinska, Belgicka, Švajčiarska, Českej republiky a Nemecka.

O spoločnosti EOS Group:

Spoločnosť EOS Group je jedným z popredných medzinárodných poskytovateľov finančných služieb na mieru. Jej hlavnou činnosťou je správa a manažment pohľadávok. S počtom zamestnancov viac ako 8 000 zaisťuje finančnú bezpečnosť pre svojich približne 20 000 zákazníkov v 26 krajinách po celom svete, a to prostredníctvom viac ako 60 dcérskych spoločností vrátane Slovenska. V rámci medzinárodnej siete partnerských spoločností EOS Group ponúka svojim zákazníkom služby vo viac než 180 krajinách na všetkých kontinentoch. Jej kľúčovými sektormi sú bankovníctvo, poisťovníctvo, sieťové odvetvia, telekomunikácie, zásielkový predaj a e-commerce. Viac informácií nájdete na: www.eos-solutions.com.